When people cite things like the AAII poll or even institutional investors’s surveys, I click off the TV. Just kidding, it’s not on to begin with. But seriously, I don’t give a shit what people say they’re doing, I pay attention to what they’re actually doing.

The Sicilians say “Watch what they do, not what they say.” They also say Asini, donni e voi, nun t’alluntanari di li toi, or “Don’t go far away from your donkeys, women and oxen”. Which is fairly sexist, but we’ll worry about that later.

Anyway, let’s just acknowledge the fact that margin debt is reaching extreme levels and just think about it psychologically – we don’t have to have a debate about whether or not this is an actionable signal.

Here’s the WSJ:

As of the end of March, the most recent data available, investors had $379.5 billion of margin debt at New York Stock Exchange member firms, according to the Big Board.

That is just shy of the record $381.4 billion in margin debt set in July 2007.

In March, the level of margin debt stood 28% higher than one year earlier, a time frame that saw the Standard & Poor’s 500-stock index rise 11.4%.

The fear is that as more investors rely on money borrowed against stocks, any significant fall in stock prices will be magnified if investors are forced to sell securities to raise cash and meet margin requirements.

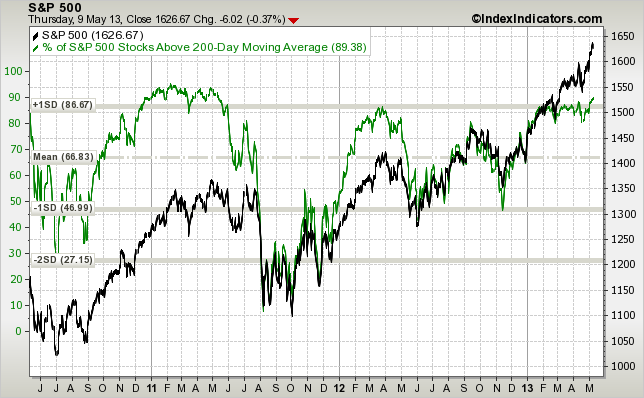

And then let’s briefly mention the extremes in market internals – a whopping 89% of the S&P 500 sits above its 200-day moving average. Again, let’s just be aware of this, we don’t have to debate it as a timing mechanism:

What I want to get across is that risk appetites are almost on full-blast. I don’t believe the margin debt we’re seeing is taking place at the retail level as during past manias. I think that’s hedge fund activity – a plus-15% S&P in the first five months of the year is mighty hard to catch up to and you know they’re killing themselves trying. Margin debt can certainly exacerbate a run of the mill sell-off, but the good news is that hedge funds typically unwind it quickly when they need to.

So the point is, don’t expect a gradual, gentle pullback if and when the Fed starts dropping hints about tapering off QE. I’d be expecting something much more sharp, short and violent. If you understand where it’s coming from, you’ll be steeled against it.

I’m a New York City-based financial advisor at Ritholtz Wealth Management LLC. I help people invest and manage portfolios for them. For disclosure information please see here.

Subscribe & Reform

Get a Full Investor Curriculum: Join The Book List

Every month you'll receive 3-4 book suggestions--chosen by hand from more than 1,000 books. You'll also receive an extensive curriculum (books, articles, papers, videos) in PDF form right away.

As of the end of March, the most recent data available, investors had $379.5 billion of margin debt at New York Stock Exchange member firms, according to the Big Board.

… [Trackback]

[…] Find More to that Topic: thereformedbroker.com/2013/05/10/two-market-extremes-you-should-be-aware-of/ […]

… [Trackback]

[…] Information on that Topic: thereformedbroker.com/2013/05/10/two-market-extremes-you-should-be-aware-of/ […]

… [Trackback]

[…] Read More on to that Topic: thereformedbroker.com/2013/05/10/two-market-extremes-you-should-be-aware-of/ […]

… [Trackback]

[…] Info to that Topic: thereformedbroker.com/2013/05/10/two-market-extremes-you-should-be-aware-of/ […]

… [Trackback]

[…] Read More to that Topic: thereformedbroker.com/2013/05/10/two-market-extremes-you-should-be-aware-of/ […]

… [Trackback]

[…] Read More here to that Topic: thereformedbroker.com/2013/05/10/two-market-extremes-you-should-be-aware-of/ […]

… [Trackback]

[…] Info on that Topic: thereformedbroker.com/2013/05/10/two-market-extremes-you-should-be-aware-of/ […]

… [Trackback]

[…] Here you will find 33811 more Information to that Topic: thereformedbroker.com/2013/05/10/two-market-extremes-you-should-be-aware-of/ […]

… [Trackback]

[…] Read More on on that Topic: thereformedbroker.com/2013/05/10/two-market-extremes-you-should-be-aware-of/ […]

… [Trackback]

[…] Info on that Topic: thereformedbroker.com/2013/05/10/two-market-extremes-you-should-be-aware-of/ […]

… [Trackback]

[…] Read More on on that Topic: thereformedbroker.com/2013/05/10/two-market-extremes-you-should-be-aware-of/ […]

… [Trackback]

[…] Find More Information here on that Topic: thereformedbroker.com/2013/05/10/two-market-extremes-you-should-be-aware-of/ […]

… [Trackback]

[…] Information on that Topic: thereformedbroker.com/2013/05/10/two-market-extremes-you-should-be-aware-of/ […]

… [Trackback]

[…] Find More Information here on that Topic: thereformedbroker.com/2013/05/10/two-market-extremes-you-should-be-aware-of/ […]